The Structural Shifts Reshaping Canada’s Pre-Construction Condo Market

Canada’s pre-construction condo market is at a breaking point and the implications extend far beyond real estate.

What was once a model built on investor confidence, early sales momentum, and steady price appreciation is now under pressure from higher rates, shifting demand, and a structural pivot toward rentals.

Don’t want to read this whole thing? Watch the video here:

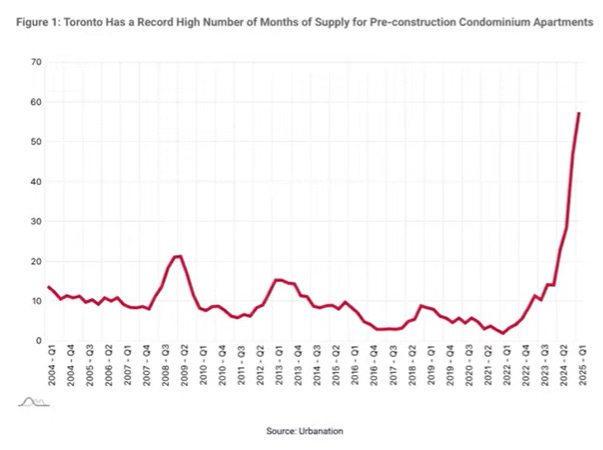

In Toronto alone, pre-construction supply has surged to 57.4 months, the highest on record. The speculative pipeline that fueled much of the past decade’s urban growth is no longer clearing, and the cost of capital is biting at both ends of the development process.

Capital at a Standstill

In development, time is money twice over. When completed units sit unsold, developers lose the ability to recycle equity into the next project. At the same time, pre-construction sales, the lifeblood of financing, have collapsed to their lowest level in over 30 years.

For the financing community, this is more than a housing story. It’s a credit flow story. Tightening liquidity in development directly impacts GDP, construction employment, and municipal revenues. And the slowdown is already measurable: 22,000 construction jobs lost according to Statistics Canada, with more pain likely if absorption rates remain weak.

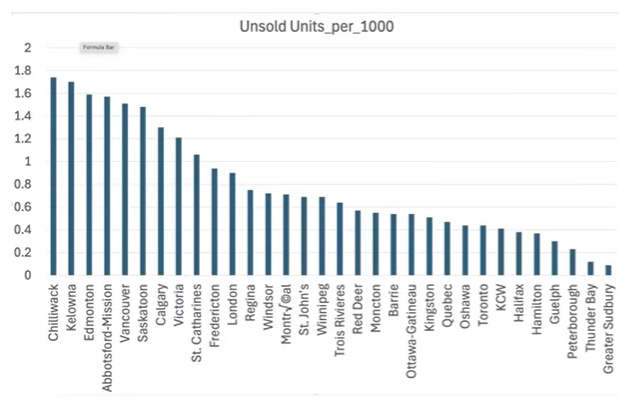

The Per-Capita Risk Lens

Absolute numbers can hide local vulnerabilities. On a per-capita basis, the most overexposed market isn't Toronto. Smaller BC cities like Chilliwack and Kelowna, along with Abbotsford–Mission and several Prairie markets, top the list:

These markets are more fragile because a single large project can swamp local demand, creating the risk of deep price discounts or stalled completions.

This matters for investors because overhangs in smaller metros often spill into surrounding areas, suppressing values regionally. Meanwhile, in Toronto, the risk is different: not a glut of unsold units, but a sold pipeline heading toward potentially cash-flow-negative closings. That creates pressure on rental yields and raises the possibility of forced sales in a higher-rate environment.

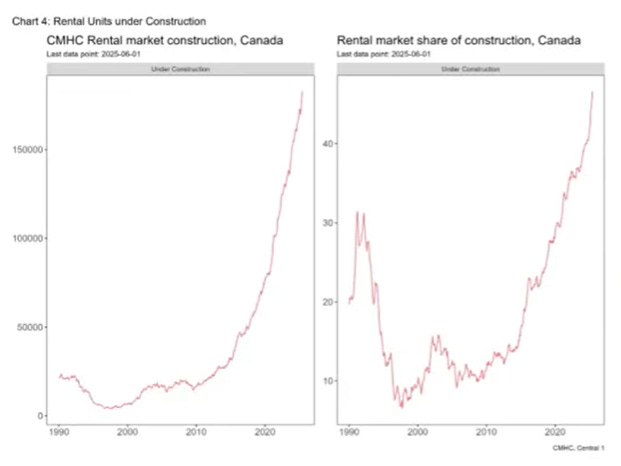

The Structural Pivot to Rentals

One of the most important and under-appreciated macro shifts underway is the redirection of capital from ownership to rental product. Rental units under construction have hit record highs, both in raw numbers and as a share of total starts.

From a capital markets perspective, this is a fundamental business model shift. The pre-con model was transactional: sell units upfront, recycle capital. The rental model is operational: retain ownership, generate long-term yield, accept slower capital recovery.

This changes how risk is distributed in the system:

Developers are holding more real estate risk on their own balance sheets.

Lenders are underwriting longer time horizons.

Investors need to re-evaluate return expectations in the face of potentially higher vacancy rates on delivery.

What to Watch Next

For those allocating capital, whether in real estate directly or in sectors exposed to construction activity, three signals matter most in the months ahead:

Absorption rates for both completed and pre-construction units in Toronto and Vancouver.

Migration and population growth trends, particularly in BC and Ontario where policy shifts are slowing net inflows.

Financing terms for multi-family development as lenders adjust to longer lease-up periods and changing cap rate assumptions.

If these indicators worsen simultaneously, we could see a second-order effect: tighter credit for developers, reduced housing starts, and paradoxically, upward price pressure once demand stabilizes, eventually.

For the complete breakdown of today’s pre-construction condo market, including more charts and regional data, read the extended blog.